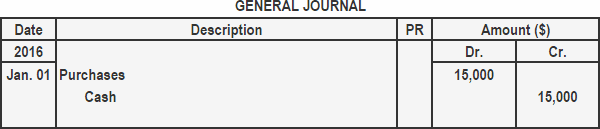

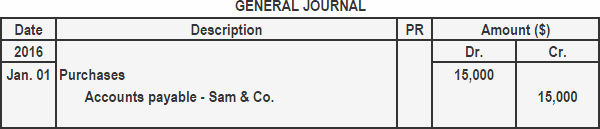

Merchandise is the term used to refer to any goods purchased for the purpose of resale in the ordinary course of business. The term is regularly used in trading organizations. Merchandise are purchased either for cash or on account. The journal entries required to record the purchase of merchandise under both the cases are discussed below: If merchandise are purchased for cash, the accounts involved in the transaction are the purchases account and cash account. The purchases account is debited and the cash account is credited. On 1 January 2016, John Traders purchased merchandise for $15,000 in cash from Sam & Co. The journal entry for this purchase is shown below. If merchandise are purchased on account, the accounts involved in the transaction are the purchases account and accounts payable account. The purchases account is debited and the accounts payable account is credited. On 1 January 2016, John Traders purchased merchandise for $15,000 on account from Sam & Co. The journal entry for this purchase would be made as follows:Merchandise: Definition

Journal Entry

When Merchandise Are Purchased for Cash

Example

When Merchandise Are Purchased on Account

Example

Journal Entry for Purchase of Merchandise FAQs

Merchandise is the term used to refer to any goods purchased for the purpose of resale in the ordinary course of business. The term is regularly used in trading organizations.

Merchandise are purchased either for cash or on account. The journal entries required to record the purchase of merchandise.

The journal entry for purchase of merchandise on account is the same as the journal entry for purchase of merchandise for cash, except that the accounts payable account is credited instead of the cash account.

The purchases account is debited when merchandise are purchased on account to indicate that an asset (the merchandise) has been acquired. The debit increases the amount of assets owned by the company.

The only difference between merchandise purchased for cash and merchandise purchased on account is the accounts involved in the transaction. When merchandise are purchased for cash, the purchases account and cash account are involved. When merchandise are purchased on account, the purchases account and accounts payable account are involved.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.