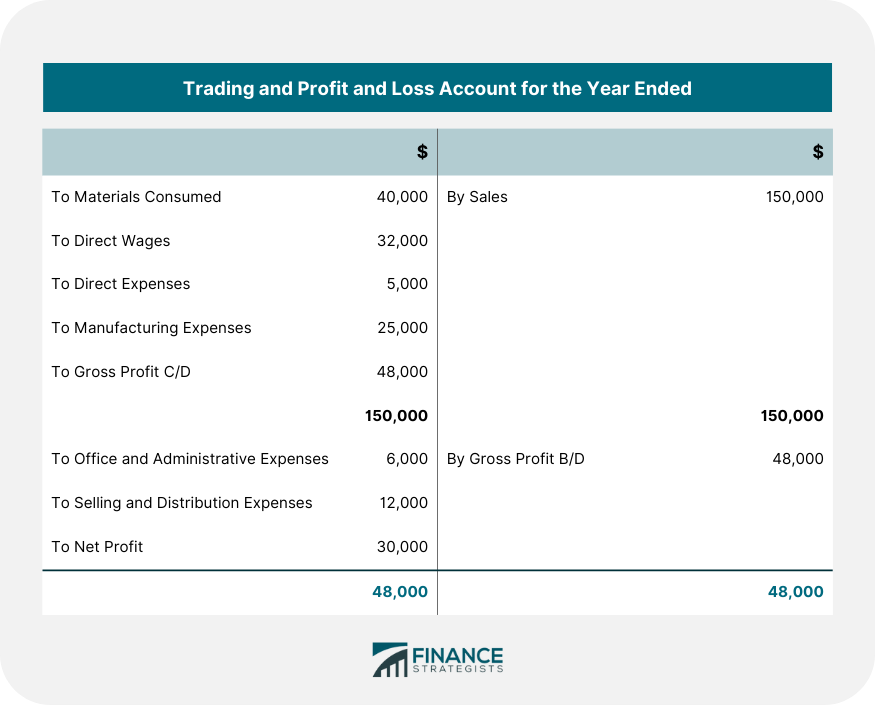

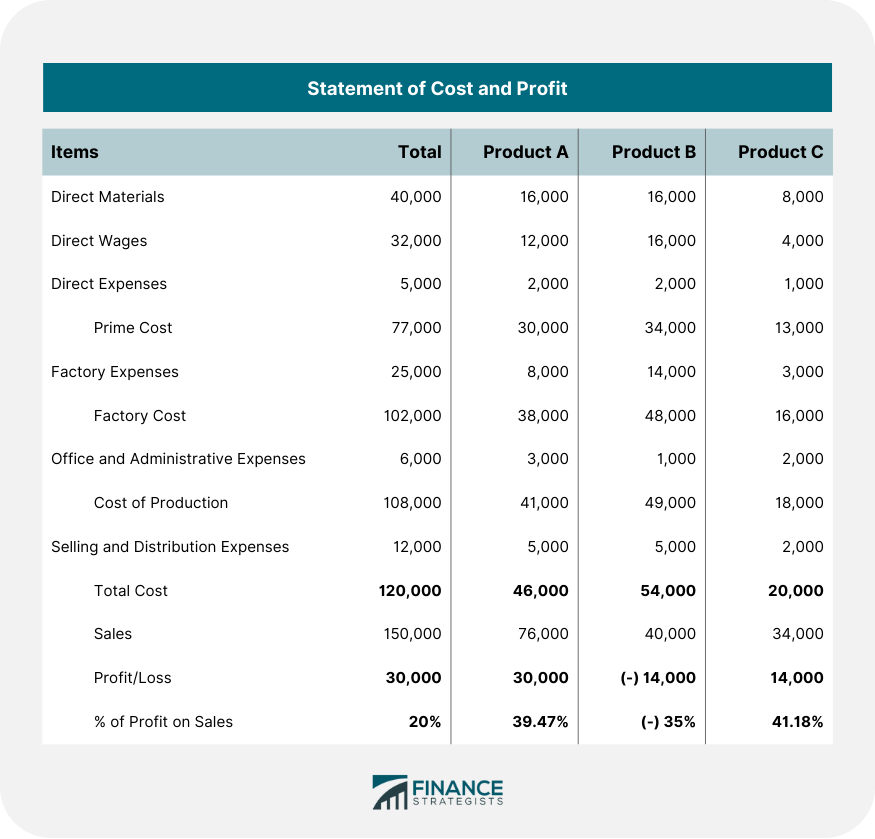

Cost accounting is closely related to financial accounting. It is generally said that the cost accounting system is complementary to the financial accounting system. According to L.W. Hawkins, an "ordinary trading account is a locked warehouse of the most valuable information, to which the cost system is the key." The trading and profit and loss account, or the financial accounts, disclose the overall profit and losses of a business for a certain period. Cost accounts throw light upon the factors that have brought about the profits or losses, as the case may be. To illustrate this fact, consider the following example: Under a cost accounting system, the company's cost accountant would present the above data in the following form: Financial accounting records show overall profitability of 20% on sales, while cost accounting records show a profit of 39.47% and 41.18% on products A and C, respectively. There is also a loss of $14,000 (35%) on product B. The cost records make it clear that a substantial part of the profits is being eaten away by product B. If management has all the necessary details, it may take the steps required to make product B a profitable one. If it is not possible, then production for product B may be halted. Therefore, while financial accounts enable managers to learn about the total profits or losses of a business concern, cost accounts—given their analytical approach—show a detailed analysis of the factors leading to such profits or losses. Cost accounts, by disclosing the factors that led to a loss, also allow managers to take the necessary steps to eliminate such losses in the future. Another important difference is that financial accounts present costs and expenses in a summarized form, whereas cost accounts present the information about these expenses in a scientifically analyzed and classified form. As a result, cost accounts are helpful for management, enabling them to learn about significant costs, areas of profitability, optimal selling prices, and improved procedures for operational planning and cost control. Therefore, it can rightly be said that the ordinary trading and profit and loss account (i.e., financial accounts) contains useful data. In addition, cost accounts supply useful details concerning the data presented in financial accounts.

Comparison Between Cost Accounting and Financial Accounting FAQs

Cost accounting is a process or system of acquiring and recording relevant and useful information about the costs incurred in manufacturing, maintaining, and servicing items for the purpose of cost analysis and control.

Financial accounting is the process of providing external users, such as investors or creditors, with informative and persuasive financial data about an entity's historical performance and condition.

Both systems attempt to provide relevant information which is useful for management purposes.

Cost accounts enable managers to learn about significant costs, areas of profitability, optimal selling prices, and improved procedures for operational planning and cost control. On the other hand, finance accounts present overall expenditures in a summarized form.

The major difference between cost accounting and financial accounting is the factor of time involved in each case.Financial accounts are prepared annually, while cost accounts are prepared more frequently to reflect current expenditures which have occurred during a certain period.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.