In current cost accounting (CCA), the cost of sales is calculated based on the cost of replacing the goods at the time they are sold. The important principle is that current costs must be matched with current revenues. Sales are current revenues and, out of the costs, all operating expenses are current costs. In the case of inventories, certain adjustments must be made, which is referred to as the Cost of Sales Adjustment (COSA). COSA can be calculated using the following formula: where Calculate the cost of sales adjustment (COSA) using the following information: To solve this, start with the COSA formula mentioned above and substitute in the correct values from the table above. In particular: COSA = (72,000 - 52,000) - 110 (72,000 / 120 - 52,000 / 120) = 20,000 - 110 (600 - 520) = 20,000 - 8,800 =$11,200 Another approach is to calculate COSA as follows: COSA = Current cost of sales - Historical cost of sales = 2,11,200 - 2,00,000 = $11,200Definition

Cost of Sales Adjustment Formula

Example

Historical Cost

Index Number

$

$

Opening Stock

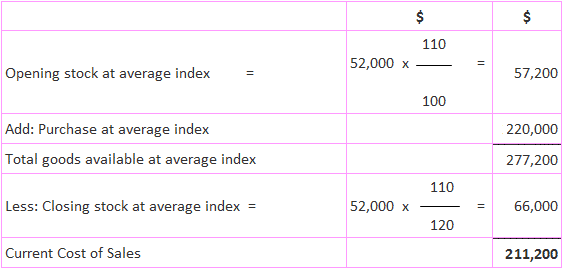

52,000

100

Purchases

220,000

110

(Average)

Total Goods

272,000

Less: Closing Stock

72,000

120

Cost of Sales

200,000

Solution

Current Cost of Sales Adjustment (COSA) FAQs

The cosa is an adjustment to the cost of sales to reflect the current costs of inventory at the time of sale. This adjustment is necessary because historical costs do not always match current costs.

A cosa must be made to ensure that the cost of sales is calculated based on the current cost of inventory. This ensures that the match between current revenues and costs is accurate.

The big idea behind the cost of sales adjustment (cosa) is ensuring that all costs are calculated based on current costs. Only in this way can accurate revenue-cost matches be made to determine profitability.

The components of cosa include the historical cost of closing stock, the historical cost of opening stock, and the average index number. Each of these components is necessary to accurately calculate the current cost of sales.

The formula used to calculate cosa is: cosa = (historical cost of closing stock – historical cost of opening stock) average index number index number appropriate to closing stock index number appropriate to opening stock

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.