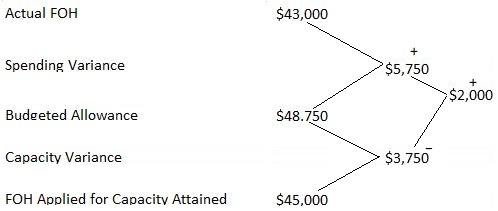

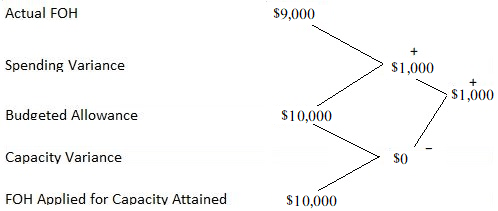

IQIZ estimated its factory overhead for the next period at $160,000. It is estimated that 40,000 units will be produced at a materials cost of $200,000. Production will require 40,000 man-hours at an estimated wage cost of $80,000. The machines will run for approximately 25,000 hours. Required: Calculate the factory overhead rate that may be used in applying FOH to production on each of the following bases: 1. Material Cost Basis Formula: = (Estimated factory overhead / Estimated material cost) x 100 = ($160,000 / $200,000) x 100 = 80% 2. Direct Labor Cost Basis Formula: = (Estimated FOH / Estimated DL cost) x 100 = ($160,000 / $80,000) x 100 = 200% 3. Direct Labor Hours Basis Formula: = (Estimated FOH / Estimated DL hours) x 100 = $160,000 / 40,000 hrs.) = $4.00 per hour 4. Machine Hours Basis Formula: = Estimated FOH / Estimated machine hours = $160,000 / 25,000 hrs. = $6.40 per machine hour 5. Units of Production Cost Formula: = Estimated FOH / Estimated no. of units = $160,000 / 40,000 hours = $4.00 per unit 6. Prime Cost Basis Formula: = Estimated FOH / Estimated prime cost = ($160,000 / ($200,000 + 80,000)) x 100 = 89% The factory overhead for the King Manufacturing Company is estimated as follows: Production for the month reached 75% of the budget. In addition, actual factory overhead totaled $43,000. Required: Calculate the following: FOH Applied Rate Formula: = FOH applied for normal capacity / Normal capacity = $60,000 (15,000 + 45,000) / 20,000 hrs. = $3 per hour Applied FOH for Actual Capacity or Capacity Attained Formula: = Actual capacity x FOH hrs. x $3 = (20,000 x 75%) x $3 = 15000 hrs. x $3 = $45,000 Budgeted Allowance Formula: = Fixed cost + Variable cost for actual capacity = $15,000 + 33,750* = $48,750 * Variable Cost for Actual Capacity Formula: = Actual capacity x Variable cost rate = 15,000 x $2.25* = $33,750 * Variable Cost Rate Formula: = Variable cost for normal volume / Normal volume = $45,000 / 20,000 hrs. =$2.25 per hour 1. Overapplied or underapplied FOH 2. Variances Spending variance Capacity variance Variance check The burden rate of John & Co. is $2.00 per hour. The budgeted overhead for 3,000 hours per month is $8,000 and at 7,000 hours is $12,000. Actual factory overhead for the month was $9,000 and actual volume was 5,000 hours. Required: Calculate the following: Formula: = Difference in burden FOH / Difference in activity level = $4,000 / 4,000 hrs. = $1 per hour Formula: = Fixed FOH Cost / Fixed FOH Cost Rate = $5,000 / $1 = 5,000 hrs. Formula: = Actual capacity x FOH applied rate = 5,000 x 2 = $10,000 Variance check Calculations Budgeted allowance: = Fixed cost + Variable cost for capacity attained = 5,000 + (5,000 x 1) = 5,000 + 5,000 = $10,000Factory Overhead Application Methods

Problem 1

Solution

FOH Variances

Problem 2

Working

Solution

High-Low Point Method

Problem 3

Solution

Activity Level

Budgeted FOH

(hrs.)

($)

7,000

12,000

3,000

8,000

4,000

4,000

1. Variable Cost Rate/V.C. in burden rate

2. Budgeted Fixed Overhead

Budgeted FOH for 7,000 hrs.

$12,000

Less VC for 7,000 hrs. (7,000 x 1)

$7,000

Fixed Cost

$5,000

OR

Budgeted FOH for 3,000 hours

$8,000

Less VC for 3,000 hours (3,000 x 1)

$3,000

Fixed Cost

$5,000

3. Normal Volume/Standard Activity Level

4. Applied Factory Overheads

5. Over- or Under-absorbed FOH

Applied FOH for Capacity Attained

$10,000

Less Actual FOH

$9,000

Overapplied FOH

$1,000

6. Capacity Variance

FOH Applied for Capacity Attained

$10,000

Less Budgeted Allowance

$10,000

7. Spending Variance

Actual FOH

$9,000

Less Budgeted Allowance

$10,000

1,000 (Favourable)

Fixed FOH Rate

Applied Burden Rate

$2.00

Less Variable Rate

$1.00

Fixed Burden Rate

$1.00

Factory Overhead: Practical Problems and Solutions FAQs

High low works best with voh because it is easy to precisely determine the difference in activity level between two months (i.E., Number of hours worked).

Using a predetermined overhead rate is better when assigning factory overheads to production in an environment where the activity levels for various products remains relatively constant even in periods of high and low sales.

A variable costing system allows companies to understand costs based on how much they are affected by sales volume. In a variable costing system, overhead costs are typically charged to expense in the period when they are incurred rather than being spread out across all units produced over a specific time frame.

Activity level is a predefined characteristic that can be applied in two different ways: an activity index or a level of capacity. These are used when allocating fixed overhead to multiple products based on the production volume associated with each unit. For example, an activity index can be calculated by dividing costs by units produced, while capacity is defined as hours worked over some predetermined time period.

Examples of allocation bases include machine hours and direct labor hours.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.