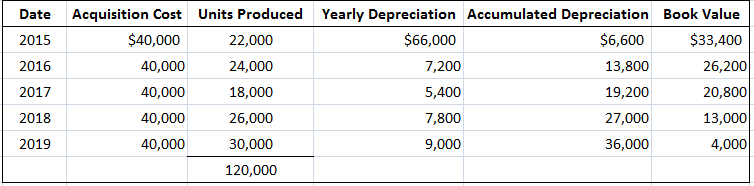

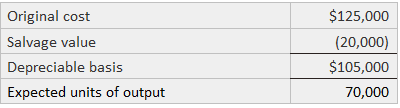

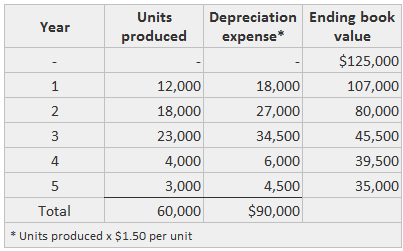

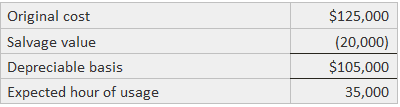

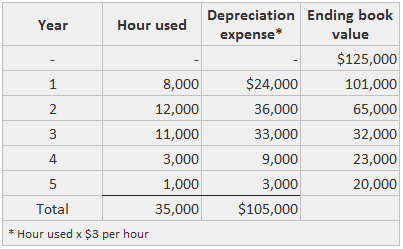

The units of production method is a method of depreciation that assumes that the primary depreciation factor is usage rather than the passage of time. It is suitable for calculating depreciation on assets such as delivery trucks and equipment for which substantial variation in usage occurs. Consider a situation in which it is economically feasible for a company to keep records relating to the quantity of output produced from an asset. If in such a situation the results of using the records are materially different from those achieved under a time-related method, the firm might use the units of output or units of production method to compute the depreciation expense. The method first computes the average depreciation expense per unit by dividing the amount of depreciable basis by the number of units expected to be produced. This per unit figure is then multiplied by the number of units produced during the time period. The cost of some assets can be allocated easily according to their estimated production or output rather than their life. The units of production method assumes that the primary depreciation factor is usage rather than the passage of time, and so it is appropriate for assets such as delivery trucks and equipment (i.e., where there are substantial variations in use). To illustrate, assume that the equipment described above is estimated to produce 120,000 units over its useful life. In this case, depreciation per unit is $0.30. To see how this is calculated, check the formula below. To calculate depreciation under the units of production method, you can apply the following formula: (Cost - Salvage value) / Estimated production in units = ($40,000 - $4,000) / 120,000 units = $0.30 per unit This cost per unit is then applied to the units produced during the year. For example, the following schedule shows yearly depreciation over the equipment's life: We assumed that the 120,000 units produced by the equipment were spread over 5 years. However, when the units of production method is used, the life in years is of no consequence. The units of production depreciation method requires that the production base, or output measure, be appropriate to the particular asset. For example, miles driven or flown might be most appropriate for a delivery truck or airplane, whereas units produced may be the most suitable for a lathe or other machine. The units of production method meets the criterion of being rational and systematic, and it provides a good matching of expenses and revenues for those assets for which use is an important factor in depreciation. However, for static assets such as buildings, the units of production method is inappropriate. The results of using the units of production method of depreciation are shown in this example for an asset with the following characteristics: Thus, the cost per unit is $1.50 ($105,000 / 70,000 units). If units of input (e.g., operating hours, materials, or labor-hours) are more descriptive than cost incurred or benefit obtained (or if they are easier to measure than units of production), the firm can use them to determine the depreciation expense. The following example shows another example application of the units of production method of depreciation. Again, the first step is the calculation of a rate by dividing the depreciable basis by the expected number of hours of operation. The example uses the same asset seen in Example 1. In this case, the rate is $3 per hour ($105,000 / 35,000 hours).Units of Production Method: Definition

Explanation of Units of Production Method of Depreciation

Formula For Depreciation Under Units of Production Method

Example 1

Units of Input

Example 2

Units of Production Method of Depreciation FAQs

The Unit of Production method is a form of Depreciation used to allocate fixed costs throughout the useful life of an asset. Fixed costs usually relate to labor and property usage, or some other measure. This allocation spreads out fixed costs across the number of units produced or used over the course of an asset's life.

To calculate Depreciation under the Units of Production method, apply the following formula: (cost - Salvage Value) / estimated production in units

The following assets typically use the Unit of Production method: delivery trucks, equipment, machinery, and vehicles.

Fixed costs are costs that remain the same even if production does not occur. If an asset has a fixed cost but no Salvage Value, then Depreciation is equal to that fixed cost each year - it makes no sense to use any other method of Depreciation (i.E., Straight-line or another accelerated method). Thus, the Units of Production method are appropriate for this type of asset.

The main advantage of this method is that it's easy to use and understand. Another advantage, as stated earlier, is that it provides a good matching of expenses and revenues for those assets for which use is an important factor in Depreciation.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.