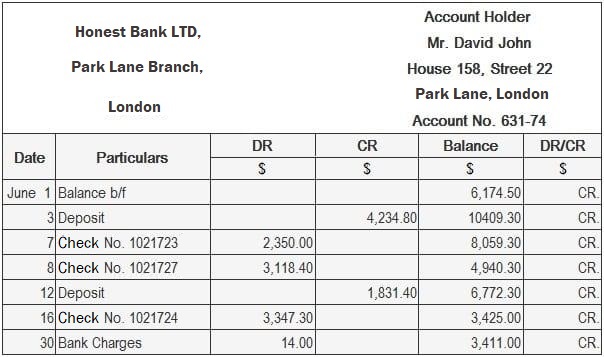

In most businesses, two or three-column cash books (with a bank column) are used to record any transactions made through the bank account. Every time cash, checks, money orders, or postal orders (or anything else) are deposited in the bank, the cash book (bank column) is debited. That's to say, an entry is made in the bank column on the debit side of the cash book. Similarly, when a check is issued to a supplier, an entry is made in the bank column on the credit side of the cash book. Just as businesses maintain cash books to stay informed about their position with the bank, the bank also maintains records to ensure that its position with the account holder is always known. On the bank's side, the record is usually kept in the form of a personal account. It is maintained more or less along the same lines as a businessperson maintains their personal accounts for debtors and creditors. As a matter of practice, banks send a list of entries to each account holder that have been made in their personal account, which is maintained by the bank. This sheet is called a bank statement. Most businesses ask for their bank statement at the end of each month. Banks use accounting machines or computers to keep their accounts. These machines usually do not follow a two-sided personal account. Instead, they use the format shown below. When an account holder deposits money with the bank, the bank's liability to the account holder is increased from the bank's point of view. You will recall that increases in liabilities are credited. Therefore, the bank credits the account holder's personal account, and the entry appears in the Cr. column of the bank statement. When an account holder issues a cheque, which the bank pays, the bank debits the account holder's personal account. In the process, this reduces the bank's liability. Thus, such entries appear in the debit column of the bank statement. Accounting machines (now computers) calculate the balance on the account after each transaction and show it in the balance column. If the balance is a Cr. balance, the last column shows 'Cr.' Alternatively, if the balance is a Dr. balance, the last column shows 'Dr.' An example of a typical bank statement is shown below. For students, it is worth noting two points in particular in this example. When David deposits money with the bank, he makes an entry on the debit side of his cash book. Additionally, the bank records all deposits received from David in the credit column of his statement of account. Can you guess the reason why? When a deposit is made by an account holder, their assets (cash at bank) increase. Hence, they make a debit entry in their cash book. However, at the same time, from the bank's perspective, a deposit received from the account holder increases the bank's liability to the account holder; therefore, the bank credits the personal account maintained for that account holder in its books. When David writes out a check, he makes an entry on the credit side of his cash book (being a reduction in asset, cash at bank). When the bank pays out cash against that cheque, it records the payment on the debit column of his statement of account. Cash Book and Bank Statement: Explanation

Bank Statement Format

Example

Cash Book and Bank Statement FAQs

In most businesses, two or three-column cash books are used to record any transactions made through the bank account.Every time cash, checks, money orders, or postal orders are deposited in the bank, the cash book is debited. That’s to say, an entry is made in the bank column on the debit side of the cash book.Similarly, when a check is issued to a supplier, an entry is made in the bank column on the credit side of the cash book.

A bank statement refers to the list of entries to each account holder that have been made in their personal account, which is maintained by the bank.

Cash book is used to record all transactions for cash, checks, money orders, or postal order while a bank statement is the list of entries to each account holder that have been made in their personal account.

The source of cash book entries are deposits received from banks, cheques issued to creditors.

The source of bank statement entries is cheques deposited by customers, payments made to suppliers by issuing a draft or check.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.