The replacement cost accounting (RCA) technique is an improvement over current purchase power (CPP). CPP suffers from the problem that it does not consider the individual price index related to the particular assets of a company. The RCA technique uses the index that is most directly relevant to the company's individual assets and not the general price index. Therefore, RCA is regarded as an improvement over CPP. Price level change can be a problem when attempting to charge depreciation on fixed assets. The aim of depreciation is to ensure that the profit and loss account is in order and to make a provision for the replacement of the fixed asset after long-term use. When depreciation is charged on historical cost, it will not match the cost of the replaced asset. To clarify, let's consider an example. Suppose a machine costs $100,000 and its lifetime is 10 years. Depreciation is charged on the original cost, which means that after 10 years, the amount is 100,000. However, the cost of the same machine due to inflation has increased to $200,000, and so a problem arises in terms of how to replace it. In this case, it is recommended that fixed assets are valued at replacement cost values. In this example, the general price index number in 2022 (i.e., the base year) is 100, 200 in 2023, and 300 in 2024. Also, the replacement costs of three assets are $80,000, $100,000, and $150,000, respectively. Required: Calculate the amount of depreciation up to 2024 on a historical cost and current purchasing power basis. Make the necessary adjustment in the ledger using the index number and replacement cost. 1. Using Index No. 2. Profit and Loss Account (Excess Dep. required on CPP basis) 3. Fixed Assets (Increased value of fixed assets on RCA basis)Overview

Depreciation and Replacement of Fixed Assets

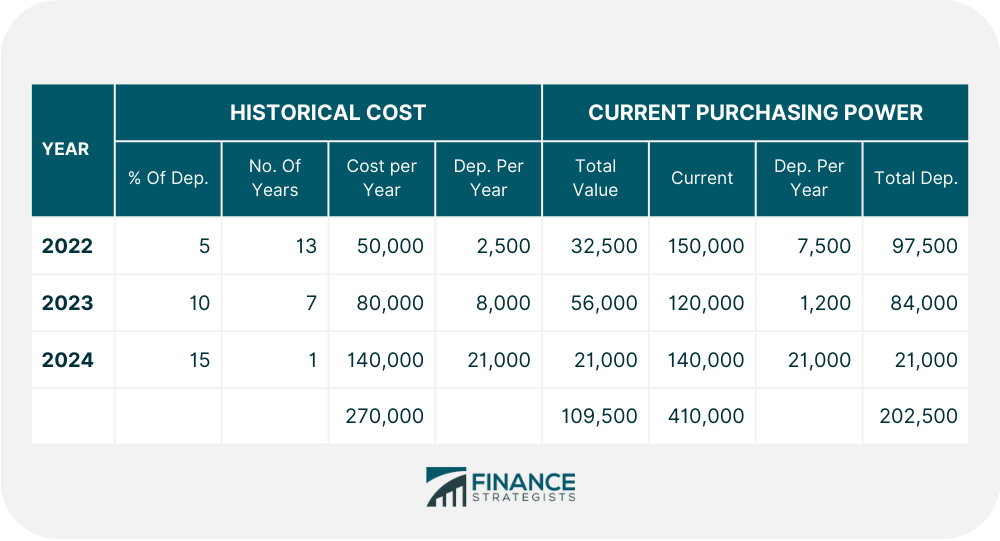

Example

Year of Purchase

Cost of Assets

Life in years

% of Dep.

2022

50,000

20

5%

2023

80,000

10

10%

2024

140,000

7

15%

Solution

Year

Historical Cost

Index

Current Valuation

$

2022

50,000

100

(50,000 x 300) / 100

150,000

2023

100,000

200

80,000 x 300 / 200

120,000

2024

140,000

300

140,000 x 300 / 300

140,000

270,000

400,000

Journal Entries

Dr.

Cr.

Fixed Asset Account

140,000

To Cap. Res. A/c

140,000

Dr.

Cr.

Fixed Asset Account

93,000

To Cap. Res. A/c

93,000

Dr.

Cr.

Fixed Assets

60,000

To Cap. Res. A/c

60,000

Replacement Cost Accounting Technique (RCA) FAQs

Replacement Cost Accounting is an improvement over current purchase power parity (cpp). Cpp suffers from the problem that it does not consider the individual price index related to the particular assets of a company. The rca technique uses the index that is most directly relevant to the company’s individual assets and not the general price index.

Rca requires the appropriate index numbers to be used when replacing old assets, which means it does not result in any loss. By using rca instead of cpp you make provisions based on the current costs the company will incur after years of use for an asset compared to the original cost of that asset.

The first step in the replacement Cost Accounting process is to identify all Fixed Assets and their corresponding original purchase price and index number. The second step is to calculate Depreciation on an annual basis, using either the historical cost or current purchasing power methodologies. The final step is to adjust the Fixed Assets account by those amounts.

The main limitation with replacement Cost Accounting is that it only works well under certain circumstances, such as when there has been no capital gains tax and indexation has not played a part in any real property investment decisions. It is also important to note that replacement Cost Accounting should not be used for intangible assets.

The key difference between replacement Cost Accounting and current purchase power parity is that cpp uses the general price index, which may not be relevant to a particular company’s assets, while replacement Cost Accounting uses the appropriate index number. This means that rca is more accurate when compared to cpp because it calculates Depreciation on the basis of current costs rather than historical costs.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.