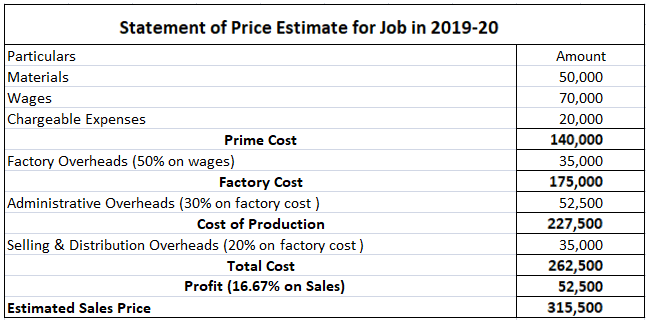

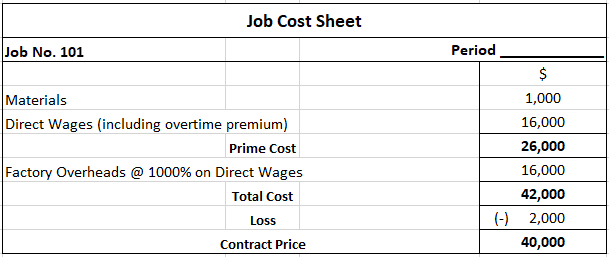

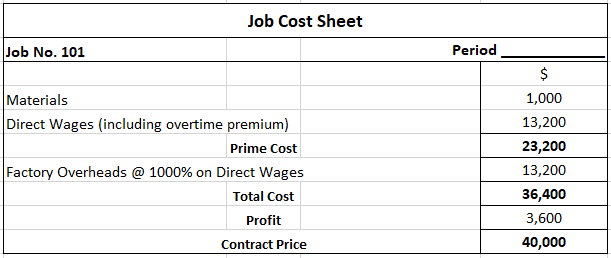

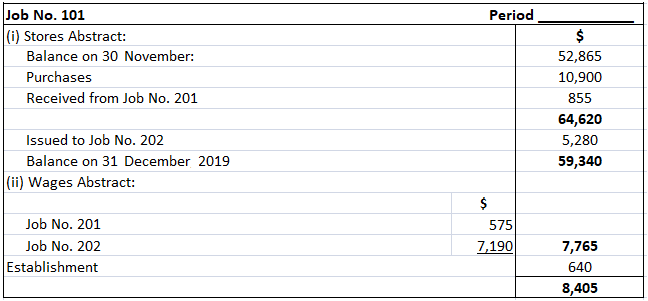

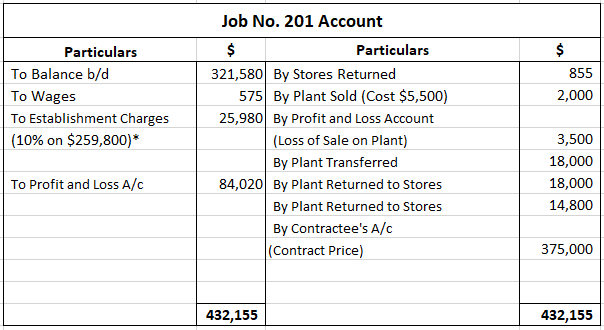

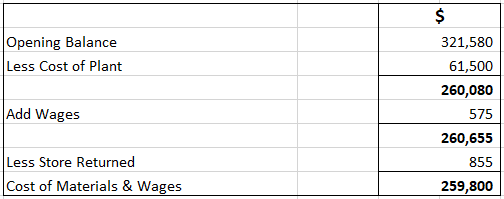

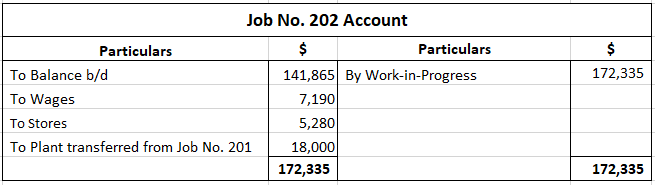

Job No. 58 passes through three departments: X, Y, and Z. The following information is given regarding this job: Required: Calculate the cost of Job No. 58 from the above figures. Note: Calculation of overheads chargeable to Job No. 58 was made as follows: The expenses shown below were incurred for a job during the year ended on 31 March 2019. The total price for the above job was $180,000. Required: The various overheads should be recovered on the following basis while calculating the estimated price: Note: Calculation of overheads rates and percentage of profit on sales took place as follows: M/s. Perfect Printers Ltd. operates a printing press. During November 2019, the plant was operating at full capacity. The material and labor costs of Job No. 101 and all other jobs worked on in November are shown below. In addition to these costs, factory overheads incurred in November amounted to $44,000. Overhead is allocated to production based on direct labor costs. Required: Factory Overhead Recovery Rate = (Factory Overhead / Direct Labor Cost) x 100 Task 1A If the overtime premium is fully charged to Job No. 101, the job cost sheet would be prepared as shown below. Task 1B If the overtime premium is charged pro-rata to all jobs, the job cost sheet would be prepared as follows: Task 2 The overtime premium should be charged fully to Job No. 101 if it was a rush job and it was done at the request of the customer. However, if the overtime work was due to limited production capacity and it was accidental that Job No. 101 was undertaken during the overtime, then the overtime premium should be charged pro-rata to all jobs. Task 3 The company's profit and loss during November will be affected by the choice of any method if all the jobs performed during the month are not completed by the end of the month. If the overtime premium is fully charged to Job No. 101 but is not completed by 30 November 2019, then the loss on the job will not be included in the account for November 2019. Similarly, if the overtime premium is charged pro-rata to all the jobs, the profit or loss on any job that remains incomplete will be carried over to the next month. The job details shown below were taken from the costing books of a contractor for the month of December 2019. The respective job accounts showed the following balances in the contract ledger on 30 November 2019. A certificate of completion was obtained for Job No. 201. Of the balance of this account standing on 30 November 2019, $61,500 was in respect of plant and machinery. The remainder consisted of wages and materials. A machine costing $5,500, specially brought for this contract, was also sold for $2,000 in December 2019. For the remainder of the balance on plant and machinery, $40,000 was used on the job for 8 months and the rest for 6 months. Of the former, 50% was transferred to Job No. 202 and the whole of the remaining plant was returned to stores. The contract price for Job No. 201 was fixed at $375,000. Required: 1. Establishment charges in respect of Job No. 201 A/c were calculated as follows:Problem 1

Solution

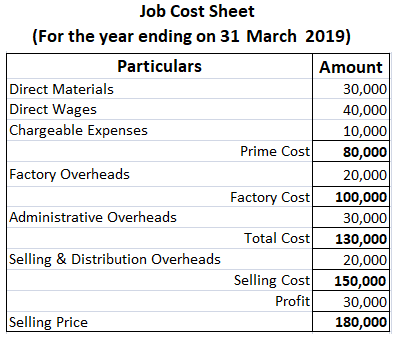

Problem 2

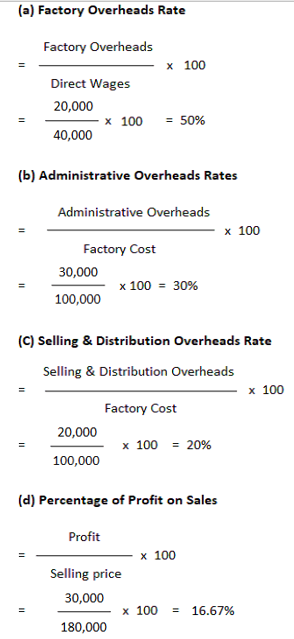

Solution

Problem 3

Solution

= (44,000 / 44,000) x 100 = 100%

Problem 4

Solution

Working

2. Depreciation on plant and value of plant returned to stores were calculated as follows:

3. A plant costing $40,000 was used for 8 months and a plant costing $16,000 was used for 6 months:

4. Half of the plant, with a total depreciated value of $36,000, was transferred to Job No. 202:

Job Costing Examples, Practical Problems and Solutions FAQs

Job costing is the method of allocating production costs to specific jobs.

A job cost sheet is prepared when the actual manufacturing costs are known. The information can be recorded in a job cost sheet which serves as a basis for charging stores, manufacturing, and administrative expenses to jobs.

Some of the main advantages of job costing over process costing include: job costing allocates overhead based on production volume, provides greater accuracy in assigning a cost to products, and differentiates between variable and fixed costs.

A job cost sheet should contain the job name, units started and units finished on each job, and direct materials used on the job

Job order costing is a method of accounting for manufacturing costs using a specially designed set of accounts. It is based on the assumption that manufacturing activities are undertaken to fulfill specific customer orders or contracts.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.