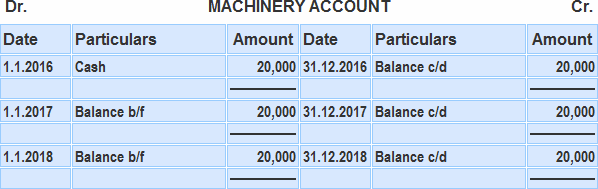

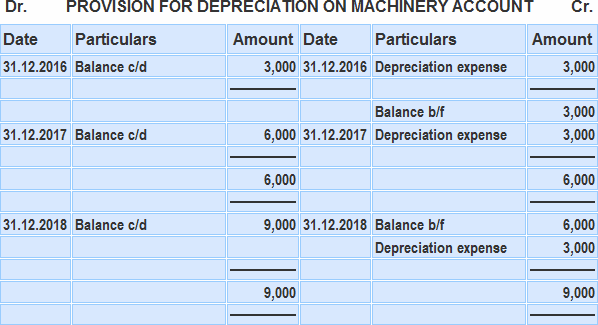

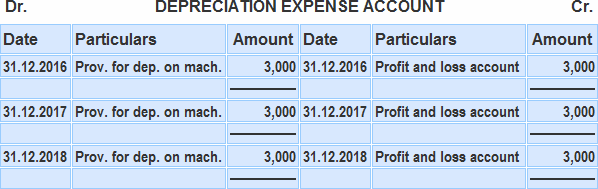

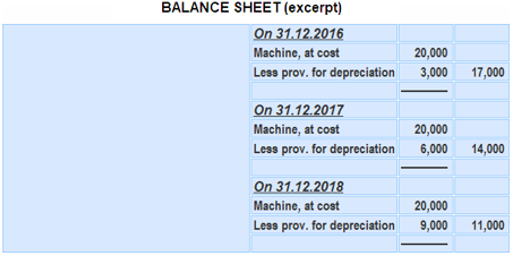

A provision for depreciation account is an improvement over the accounting treatment of depreciation. This account is used to accumulate depreciation that is provided against a fixed asset. If a provision for depreciation account is used, the accounting entries are made as follows: One provision for depreciation account is opened for every fixed asset account. For example, for a motor vehicle account, a "provision for depreciation on motor vehicle account" will also be opened. Similarly, for plant and machinery, there will be a "plant and machinery account" and also one "provision for depreciation on plant and machinery account". At the end of each financial year, debit the depreciation expense account and credit the provision for depreciation (on relevant fixed asset account) with the amount of depreciation calculated for the year. Debit the depreciation expense account Credit the provision for depreciation on the relevant fixed asset The balance in depreciation expense account is transferred to the profit and loss account at the end of the year. The balance of the provision for depreciation account is carried forward to the next year. Note that the provision on depreciation account is not a nominal account, it is a part of the asset account. Also note that it will always show a credit balance that will increase each year. At any given time, the balance on a provision for depreciation account represents the total accumulated depreciation that has been provided against a particular asset. No entry relating to depreciation is made in a fixed asset account. This account will continue to show a debit equal to the cost of the fixed asset concerned. The only entries that will be made in the fixed asset account will be in respect of fresh purchases or sales of the asset concerned. The formula for the book value of a fixed asset is the following: Book value = Cost (per fixed asset account) - Accumulated depreciation (per provision for depreciation account) Although one depreciation account is enough to accommodate the depreciation expense on all fixed assets for the year, a separate provision for the depreciation account must be maintained for each fixed asset account. If a fixed asset is recorded using the revaluation approach for calculating depreciation, it is usually not necessary (or beneficial) to maintain a separate provision for depreciation account for it. For such assets, the treatment shown on the revaluation method is sufficient (i.e., depreciation may be directly credited to the fixed asset account). PQR company bought a machine for $20,000 on 1 January 2005. The company uses the fixed installment method of depreciation and estimates that the machine will have a useful life of 6 years, leaving a scrap value of $2,000. Required: Show the relevant ledger accounts for the years 2016, 2017, and 2018. Step 1: Compute depreciation for each year Depreciation per year = (Cost - Scrap value)/Useful life of the asset = ($20,000 - $2,000)/6 = $3,000 The depreciation charge for each of the six years of the machine's useful life is $3,000. Step 2: Preparation of ledger accounts Keeping a separate provision for depreciation account for each fixed asset offers the following advantages: 1. As no entry is made in the fixed asset account, it continues to show the historical cost of the asset. The historical cost of a fixed asset is needed for a number of reasons, such as computing depreciation using the fixed installment method (also known as the straight line method) or the payment of rates and taxes. If depreciation is credited directly to the fixed asset account, it may be difficult to determine the asset's historical cost after a few years. 2. A separate provision for depreciation account ensures that the total accumulated depreciation is always known for each fixed asset. This helps to determine the fixed asset's book value. It also provides an idea about the age of the fixed assets that are held. Therefore, if the total cost of the fixed assets is, for example, $4,000 and the total provision for depreciation stands at $3,200, it can be seen that the fixed assets are nearing their useful life. Significantly, knowing only the book value of $800 ($4,000 - $3,200) cannot provide this level of insight. 3. When fixed assets are revalued (for whatever reason), it is always helpful to know both the original cost and accumulated depreciation of each fixed asset. Maintaining a separate provision for depreciation account also makes this possible.Entries in Provision for Depreciation Account

Entry 1

Entry 2

Entry 3

Entry 4

Entry 5

Entry 6

Entry 7

Entry 8

Example

Solution

Advantages of Using a Separate Provision for Depreciation Account

Exercises

Provision for Depreciation Account FAQs

A provision for depreciation account is an improvement over the accounting treatment of depreciation. This account is used to accumulate depreciation that is provided against a fixed asset.

First, as no entry is made in the fixed asset account, it continues to show the historical cost of the asset. A separate provision for Depreciation accounts ensures that the total accumulated Depreciation is always known for each fixed asset. Lastly, when fixed assets are revalued (for whatever reason), it is always helpful to know both the original cost and accumulated depreciation of each fixed asset.

You must decrease the value of an asset by the amount of depreciation and increase the balance for accumulated depreciation. The difference between the decrease and the accumulated depreciation is transferred to the income statement.

Provision for depreciation is required in a business to determine actual profit and loss. The following are some of the reasons why: 1) Since depreciation of an asset constitutes a decrease in its value, profits must be adjusted to allow for the depreciation suffered during the period. 2) Failure to include provisions for depreciation may result in the sale price including an artificially high profit for the business.

A depreciation provision allows a company to account for the gradual decline in the value of its fixed assets over time, thus allowing the company's financial statements to accurately reflect the current value of its investments in those assets.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.