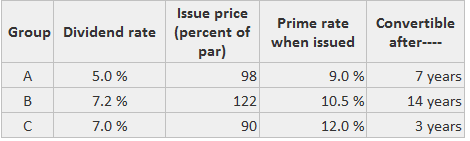

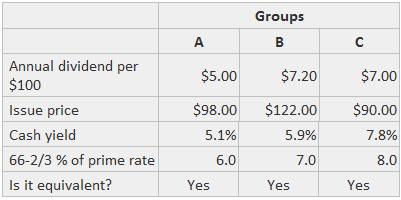

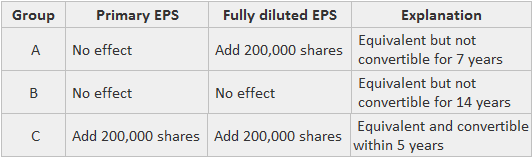

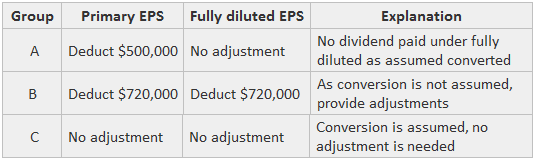

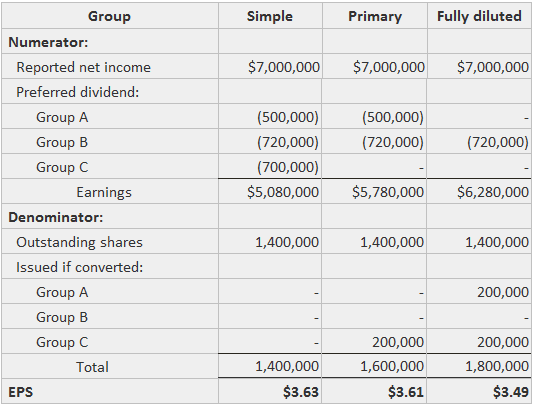

The general treatment of convertible preferred stock in earnings per share (EPS) calculations is basically identical to that used for convertible bonds. Common stock equivalency is determined by comparing the cash yield at issuance to 66 2/3 percent of the prime rate. If designated as an equivalent, it is treated that way as long as it is outstanding. If it is necessary to assume conversion of preferred stock, an accountant must increase the denominator by the number of common shares that would have been issued. The treatment for the numerator is different from the one used for bonds because the preferred dividends are not a factor in the calculation of net income. If conversion is not assumed, the dividends on the preferred shares are deducted from net income to determine the earnings available to common stockholders. On the other hand, if conversion is assumed, the dividends would not have been paid and, accordingly, are not deducted from net income. Given that dividends are not deductible expenses for tax returns, there is no adjustment to the dividends for additional taxes. For primary EPS, conversion is only assumed for convertible preferred stock that satisfies the following criteria: The stock is considered to be equivalent to common shares The stock is actually convertible within the next five years For fully diluted EPS, conversion is assumed for all preferred shares that are convertible within the next 10 years. Preferred shares are anti-dilutive if the dividends saved per issuable common share exceed EPS without assuming conversion. Suppose that the Sample Company has three issues of convertible preferred shares outstanding. Each has a par value of $10,000,000 and is convertible to 200,000 shares of common stock. The following facts are known about each group: The test for equivalency is shown below: The impact on EPS denominators is presented as follows: The reported net income will receive these adjustments: The EPS calculations are presented below, including simple EPS. This is done to show the treatment of preferred dividends and the extent of dilution (the net income and outstanding shares are assumed). If convertible preferred shares are converted during the reporting period, earnings per share (EPS) figures are calculated as if they were converted at the beginning of the period. Therefore, the numerator is not adjusted for the preferred dividends that are actually paid during the part of the year in which they were outstanding. The number of common shares issued at conversion is included in the weighted average of outstanding shares. For the period prior to conversion, the common shares that would have been outstanding are weighted by the appropriate fraction of the year. For newly-issued convertible preferred stock, any adjustment to the numerator is limited to the number of dividends actually declared (or accumulated). Under the assumption of conversion, the number of issuable common shares is weighted by the fraction of the year that the preferred stock was outstanding.Explanation

Impact on EPS

Example

Conversion or Issuance During the Period

Convertible Preferred Stock Impact on EPS FAQs

No, however an adjustment will have to be made in the numerator. To determine this, assume that conversion did not take place and calculate the diluted earnings per share (eps) accordingly. Once you have done this, then assume that the conversion did take place and calculate eps accordingly.

Preferential dividends, i.E., Those greater than a non-preferred dividend, are not deducted from net income to determine earnings available to common stockholders or from common stocks if it is assumed that the preferred shares are converted.

Conversions and issuances during a reporting period will have an impact on eps if it is assumed that they were in place for the entirety of the year. To determine the number of issue shares attributable to this, calculate earnings per share (eps) for the part of the year in which the convertible preferred stock was not outstanding. Then factor in any dividends that would have been paid with each additional common share over this period. Finally, assume that these shares were converted or issued and calculate eps accordingly.

If it is assumed that convertible preferred stock will be converted within the next 10 years, the number of issuable common shares would decrease by the appropriate fraction. Therefore, the diluted eps denominator would be reduced accordingly.

No, to determine diluted eps for convertible preferred stock dividends paid on them will not be deducted from net income. Dividends paid on the convertible preferred would reduce the amount to be distributed as a dividend and therefore reduce the number of shares that need to be included in the denominator.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.