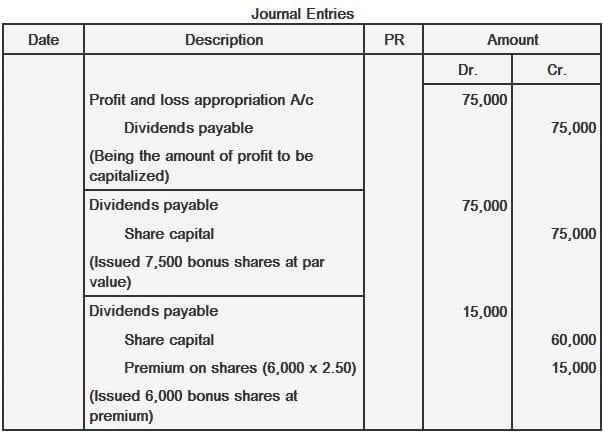

A company's undistributed profit is transferred to the profit and loss appropriation account or retained earnings. If the directors decide that a portion of the profit will be divided among the shareholders, the following journal entry would be made: To retain cash in the business, the directors may decide to issue shares to shareholders. The shares issued are known as bonus shares. In this way, shareholders will receive additional shares without making any further payment. The issue of bonus shares in payment of dividends is called capitalization of un-distributed profit. The following accounting entry is made for the issuance of bonus shares: If shares are issued at a premium, the accounting entry would be: Delight Corporation Limited shows a retained earnings balance of $185,000. The directors decided to capitalize $75,000. Required: Prepare separate journal entries under each of the following assumptions. Explanation and Journal Entries

Profit and Loss Appropriation/Retained Earnings ------------------Dr.

Dividends Payable ----------------------------------------------------------------Cr.

Dividends Payable ---------------------------------- Dr.

Share Capital ------------------------------------------Cr.

Dividends Payable ------------------------------- Dr.

Share Capital ---------------------------------------Cr.

Premium on Shares ------------------------------ Cr.

Example

Solution

Issue of Bonus Shares FAQs

A bonus issue is a type of share issuance where a company issues additional shares to its shareholders above and beyond the number of shares that they already own.

When a company issues bonus shares, the value of the shares is recorded as a liability on the company's balance sheet. This is because the company has incurred an obligation to give away additional shares to its shareholders. The amount of this liability will be based on the fair market value of the shares at the time of issuance.

The bonus issue of shares is usually calculated as a fixed percentage of the total number of outstanding shares. For example, a company might issue an extra 1% of shares to its shareholders for every 100 shares they already own. This would mean that if you held 1000 shares in the company, you would receive an extra 10 shares as a bonus.

One reason could be to raise money for the company, as issuing additional shares will result in more cash being raised. Another reason could be to reward shareholders for their loyalty or to increase the number of shares outstanding so that the company can be more easily bought or sold.

The process of issuing Bonus Shares involves seeking approval from shareholders through an Extraordinary General Meeting (EGM), notifying stock exchanges about the same, and ensuring compliance with other applicable laws. The company then issues additional shares as per a predetermined ratio post issue of board resolution and necessary filings to exchanges/registrar accordingly.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.