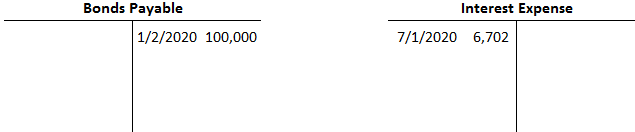

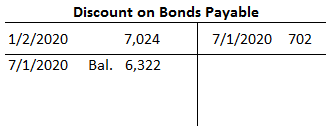

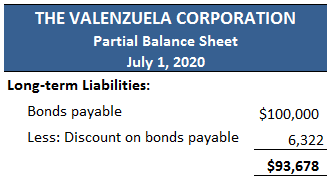

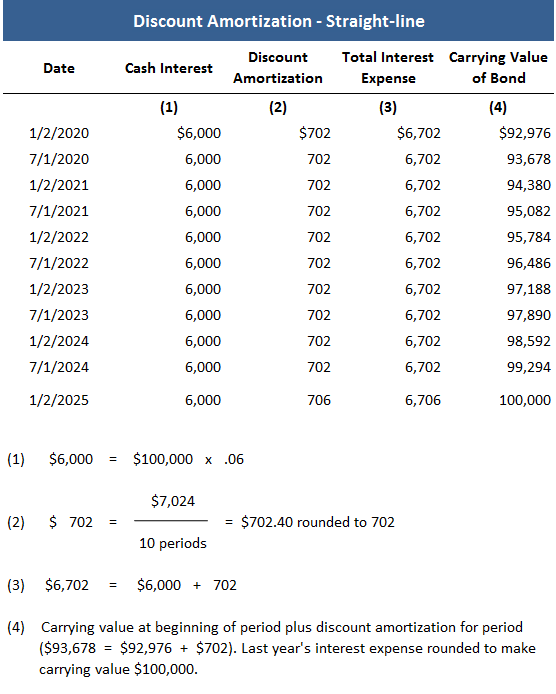

The straight-line method of amortization allocates the discount evenly over the life of the bond. There is a constant interest charge each period. An entry is usually made on every interest date, and if necessary, an adjusting journal entry is made at the end of each period to record the discount amortization. To demonstrate the use of the straight-line method, we will return to the Valenzuela Corporation example. In this case, the discount of $7,024 is amortized over 10 interest periods at a rate of $702 per interest period ($7,024 / 10). The total interest expense for each period is $6,702, which consists of the $6,000 cash interest and the $702 amortized discount. Another way to calculate the $6,702 is to divide the total interest cost, $67,024, into the 10 interest periods of the bond's life, as in the journal entry for 1 July 2020. The same is done for each subsequent payment date. As the bonds approach maturity, their carrying value increases. The result of this, as well as subsequent entries, is to reflect the increase in the carrying value of the bonds. This is attributable to the discount account, which is offset against bonds payable in arriving at the carrying value (this decreases every time a credit entry is made to that account). To illustrate, the relevant T-accounts and a partial balance sheet as of 1 July 2020 are presented below. In each interest period, the bond's carrying value increases $702, so that by the time the bond matures, the balance in the Discount on Bonds Payable account will be zero, and the bond's carrying value will be $100,000. Exhibit B below shows an amortization schedule for this bond on the straight-line method. When the company repays the principal, it will make the following entry: Exhibit BStraight-Line Method of Amortization: Definition

Application of the Straight-Line Method

Straight-Line Method of Amortization FAQs

The straight line method of amortization allocates the discount equally over the life of the bond. There is a constant interest charge each period. An entry will usually be made on every interest date and if necessary, an adjusting journal entry will be made at the end of each period to record the discount amortization.

It's usually applied by using the following formula: Amt = P x (1 - (1/Y)) where, P- Principal amount on issuance =, Y- Number of years to maturity, Amt- Amortization amount

In this case, the company can make a lump sum payment rather than several smaller payments. This leads to saving in interest costs and also helps in making a smooth transition from one accounting period to another. Further, companies can pick up the coupon payments in advance and reduce their interest costs.

If a company's profits are unstable, it may choose to use this method of amortization which will help them avoid paying tax on periodic basis.

The carrying value of the bond will increase at every interest date by the same predetermined amount irrespective of when payment is actually made. The result of this, as well as subsequent entries, is to reflect the increase in the carrying value of the bond.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.