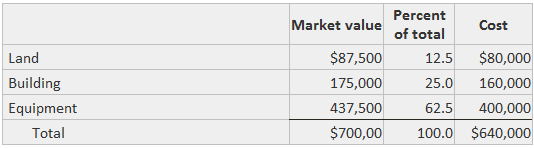

Since almost every type of asset can be viewed as a set of components, there are very few situations in which a single asset is acquired. In many (if not most) cases, this fact is ignored because the components are either permanently joined together, share the same useful life, or information about the separate components is not relevant. However, in other cases, it may be useful to recognize the separate parts of an asset in order to determine and report the cost of using each part over the course of their unique service lifetimes. To accomplish this separation, it is necessary to allocate the cost of the package of assets among the separate items in accordance with some logical allocation basis. Suppose that an existing factory is purchased for a single sum of $640,000. This price includes the land deed, a building, and the equipment in the building. To calculate depreciation, it is necessary to subdivide the $640,000 across the three main items. A widely used reasonable allocation basis is the assets' relative market values. Assume that a pre-purchase appraisal worked out the following market values for the respective assets if purchased separately: The total cost would be allocated in accordance with the following schedule: If the total cost exceeds the total market value of the identifiable assets when an entire company is being purchased, there is evidence that goodwill exists, and this allocation procedure should not be used.Definition and Explanation

Example

Acquisition of Multiple Assets Together FAQs

The term 'acquisition of multiple assets' refers to the purchase or obtaining of multiple things at once.

It's important because you want to make sure that you are properly accounting for all costs associated with the sale of your company. If any money is being made off of the goodwill you have built up, it can be considered taxable. The IRS has strict guidelines on how to handle proper accounting for these transactions.

This happens when a person purchases multiple assets which are generally obtained at once. This could include real estate taken over by a company, the purchase of multiple items at once such as a car lot, and even when an individual purchases more than one item at one particular time.

This applies most commonly when a person is purchasing a lot at once for several things they want to build on it or is taking over multiple properties which are all located together. It also applies when an individual has made purchases more than one item at once, such as if they were purchasing multiple cars.

The main advantage is that you will know for certain if there is any taxable income coming from the goodwill you have built up over time.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.