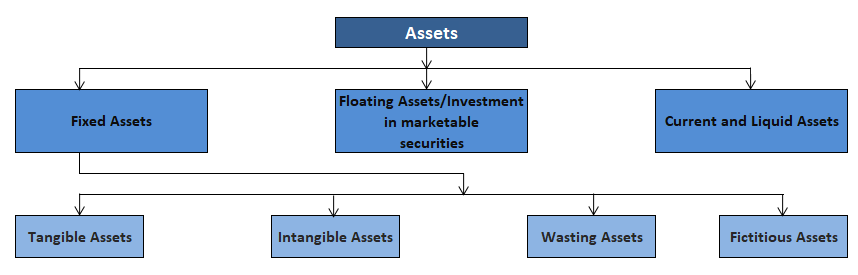

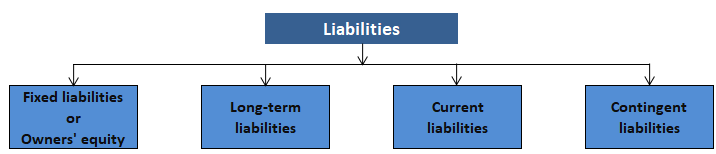

A balance sheet is a statement that outlines the financial position of an enterprise. It is necessary for the balance sheet to show the enterprise’s assets and liabilities based on their characteristic features. If assets are the property and possessions of the business, liabilities are its legal obligations (i.e., the claim by outsiders on the assets of a business). (No doubt, the Owner’s equity is also a liability that the business owes to the proprietors or partners.) Assets may be broadly classified into three categories as shown in the below figure. Fixed assets can be divided into the following groups: Fixed assets are assets acquired for beneficial use and held permanently in the business. The business can earn profits by using these assets. Tangible assets (or definite assets) are fixed assets that can be seen and touched, and which have volume. Examples of tangible assets include land, antiques, plants, buildings, fixtures, vehicles, and equipment and tools. Intangible assets are assets that cannot be seen or touched, and which have no volume. Examples include goodwill, patents, trademarks, copyrights, and leaseholds. Wasting assets are assets that get exhausted or reduce in value when used. Natural resources, oil, timber, coal, mineral deposits, and quarries are all examples of wasting assets. Fictitious assets are assets that are either past accumulated losses or expenses, which are incurred once in the lifetime of a business and are capitalized for the time being. These items are not actually assets but are treated as assets. Due to the intangible nature of fictitious assets, they are sometimes also categorized as intangible assets. Examples of fictitious assets include organizational expenses, discounts on issues of shares, advertising expenses capitalized, and research and development expenses. Investments in short-term marketable securities that can quickly be converted into cash can be treated as current assets, whereas investments in long-term marketable securities can be treated as semi-fixed assets. Therefore, some investments cannot be categorized either as current assets or fixed assets. Their treatment differs depending on their nature and, hence, they are shown midway between fixed assets and current assets, and are considered floating assets. Current assets are expected to be sold or otherwise used up in the near future. These assets are readily available for discharging an enterprise's liabilities. Those items of assets which can be converted into cash quickly without significant loss of time and money are called liquid assets and fall under the category of current assets. Examples of current assets include cash, bank balance, accounts receivables (sundry debtors and bills receivables), and stock that can be realized quickly. Liabilities may be classified into four categories, as shown in the figure below. Fixed liabilities are due to the owners/partners/shareholders of an enterprise, and they are payable only on dissolution/liquidation of the enterprise. These are in the nature of long-term loans (e.g., 5-10 years) or debentures that are payable on or after the lapse of the term consented to in the borrowing agreement/document. These are short-term obligations payable within the next accounting period/year or payable within a very short period (e.g., 1-3 months). Examples of current liabilities include accounts payable (sundry creditors and bills payable), short-term bank overdrafts, and short-term temporary loans. Contingent liabilities arise depending on the happenings of certain events. Such liabilities may or may not arise. However, it is important to be cautious about them. Consider the example of a case that is pending in a court of law concerning a disputed payment or compensation claim. If the case is decided against the enterprise, then liability arises. Otherwise, there is no obligation to pay and, as such, no liability. Bills discounted, as well as guarantees given against loans from another enterprise or person, may also cause liability if the other person does not honor the commitment. If the person honors the commitment, then no liability arises. This means that the liability is 'probable'. Probable liabilities are treated as contingent liabilities, and a note is given for such liabilities below the balance sheet. This note helps the information users to make a proper decision. What Are Assets and Liabilities?

Classification of Assets

1. Fixed Assets

2. Floating Assets

3. Current Assets

Classification of Liabilities

As indicated above, liabilities can be divided into the following groups:

1. Fixed Liabilities

2. Long-Term Liabilities

3. Current Liabilities

4. Contingent Liabilities

Classification of Assets and Liabilities FAQs

Assets and liabilities can be classified as follows: intangible assets, Fixed Assets, current assets, floating assets, current liabilities, long-term liabilities, contingent liabilities.

Some investments can be treated as either current or fixed. These are called floating assets.

Cash, bank balance, and other forms of current assets are readily available for use; hence they are called current assets. Accounts Receivable (sundry debtors and bills receivable) and stock received from the customers that have not been sold yet and which cannot be converted into cash quickly without significant loss of time and money fall under the category of current assets.

Liabilities may be divided into the following groups: fixed liabilities, long-term liabilities, current liabilities, and contingent liabilities.

Contingent liabilities arise depending on the happenings of certain events. Such liabilities may or may not arise. However, it is important to be cautious about them.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.