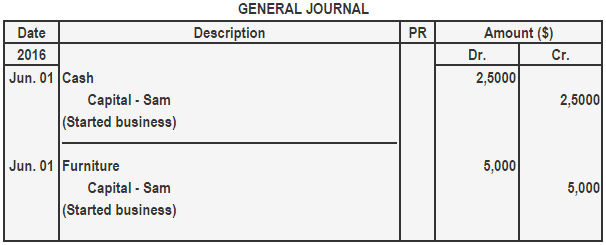

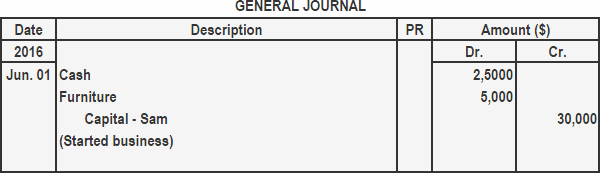

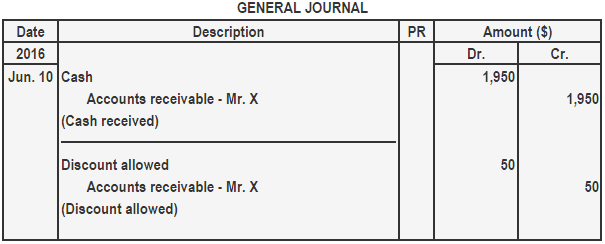

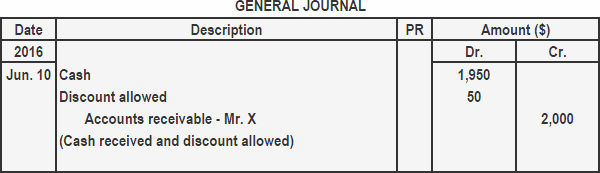

A compound journal entry is a journal entry that involves more than two accounts. When two or more transactions of the same nature take place on the same date, accountants prefer to make a compound journal entry instead of two or more separate journal entries. There are two conditions to satisfy in a compound journal entry: In a compound journal entry, debit, credit, or both parts of the entry consist of more than one account. On 1 June 2016, Sam started a business with $25,000 in cash, along with furniture costing $5,000. The above transaction consists of three accounts: cash account, furniture account, and capital account. These transactions can be journalized by making either two separate journal entries or one compound journal entry. Both the methods are illustrated below. On 10 June, Sam received $1,950 in cash from Mr. X, a customer. Mr. X was allowed a cash discount of $50. The above transaction also has three accounts: cash account, accounts receivable, and discount allowed account. Again, Sam has the option to make two separate journal entries or a compound journal entry.Compound Journal Entry: Definition

Example 1

If two separate journal entries are made:

If a compound journal entry is made:

Example 2

If two separate journal entries are made:

If a compound journal entry is made:

Compound Journal Entry FAQs

Compound journal entries are preferred because, in accounting, it is desirable to avoid making more than one entry for the same transaction.

Yes! A single account can have more than one debit or credit part. The account can have debit or credit part, or it can have both debit and credit parts. But the sum of debit and credit parts should be equal to the amount of the account. Thus, in a compound journal entry, if there is more than one account involved then at least one of them will have more than one debit or credit part.

Yes! The amount of debit or credit parts in a transaction is not required to be equal, but their total amount should add up to the total amount of the account being debited or credited.

Yes! We can certainly have a compound journal entry with an allowable account. An allowable account is created for allowing certain amounts in our books of accounts beyond actual transactions. This kind of accounts is called allowance account.

Yes! We can certainly link two or more accounts when we make a compound journal entry. Linked accounts, if any, will be debited and credited in the same part of the entry.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.