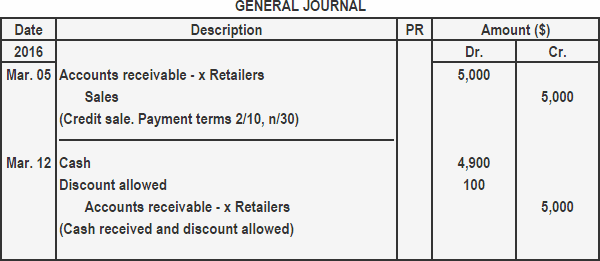

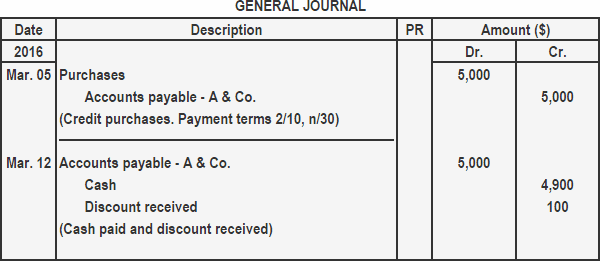

A cash discount may be offered by a seller to a buyer to encourage them to make a payment within a desired number of days. The purpose of cash discount is to encourage buyers to make payments before the due date. The percentage of cash discount is mentioned in the payment terms. For example, the terms 2/10, n/30 mean a 2% discount will be allowed if the payment is made within 10 days of the date of invoice; otherwise, the full amount is to be paid in 30 days. Cash discount is an expense for the seller and income for the buyer. It is, therefore, debited in the books of the seller and credited in the books of the buyer. On 5 March 2016, A & Co. sold merchandise to X Retailers for $5,000 on credit. A & Co. grants a 2% discount to all credit customers if the payment is made within 10 days of the date of invoice. X Retailers made the payment on 12 March 2016 and received a cash discount, as promised by the seller. Required: 1. Entries in seller's books (A & Co.) 2. Entries in buyer's books (X Retailers)Cash Discount: Definition

Journal Entry for Cash Discount

Example

Solution

General Journal Exercises

Journal Entry for Cash Discount FAQs

A cash discount may be offered by a seller to a buyer to encourage them to make a payment within a desired number of days. The purpose of cash discount is to encourage buyers to make payments before the due date.

The percentage of cash discount is mentioned in the payment terms. For example, the terms 2/10, n/30 mean a 2% discount will be allowed if the payment is made within 10 days of the date of invoice; otherwise, the full amount is to be paid in 30 days.

Cash discount is an expense for the seller and income for the buyer. It is, therefore, debited in the books of the seller and credited in the books of the buyer.

Giving cash discounts is just one of the many ways to cultivate better business relations with your buyers.

1. Pass journal entries in the books of the seller at the time of the sale of merchandise and collection of cash., 2. Pass journal entries in the books of the buyer at the time of purchase of merchandise and payment of cash

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.