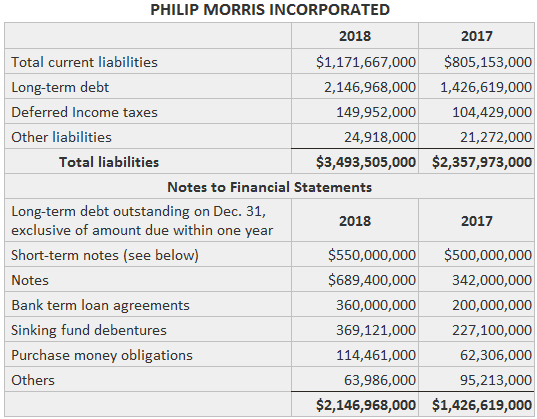

As the maturity date of a liability approaches, the working capital available for other uses is reduced. On the other hand, if the maturity date is in the distant future, the firm can commit its resources to long-run strategies. Thus, information about the remaining time to a liability's maturity may help assess both solvency and earning power. The GAAP call for classifying liabilities as either current or non-current according to their due dates. It indicates that a liability is to be treated as current if it falls due in the next 12 months or the operating cycle, whichever is longer. All other liabilities are non-current, with the exception of two items discussed below. When a single liability has payments falling due over several years, those payments due within one year (or a longer operating cycle) are classified as current. When one of these payments is reclassified from non-current to current, no journal entry needs to be made, although the action must be disclosed on the statement of changes in financial position (SCFP) as a use of working capital. Two exceptions to the classification scheme are encompassed in the GAAP. First, liabilities are excluded from being classified as current if they are to be satisfied with non-current assets (e.g., cash held in a sinking fund). The second exception relates to liabilities that are to be refinanced. In these cases, the liabilities do not need to be classified as current even if they are due within the next year or operating cycle. In this context, the term "refinanced" means replaced with other debt (either by extending the due date of the existing loan or borrowing cash to repay it) or with equity (either by conversion or by issuing shares to obtain the cash to pay off the debt). The major consequence of these actions is the avoidance of a reduction of working capital. There may be two conditions under which this exception can be applied. Specifically: The statement further identified characteristics that the agreement must have: The purpose of the two exceptions to the classification of current liabilities (for payments with non-current assets and refinancing) is to avoid misleading statement readers concerning the firm's short-run solvency. Because the firm's real working capital is not impaired by the payment of these liabilities, the statements should present a more appropriate picture. The following example illustrates a disclosure from the published financial statements for Philip Morris Incorporated. Short-term obligations are shown as non-current because they are to be refinanced. The company has entered into a $300,000,000 revolving credit and term loan agreement, maturing in 2021, and a $250,000,000 Eurodollar revolving credit agreement maturing in 2022. Both of these agreements can be used to refinance short-term notes payable. Management intends to exercise its rights under these agreements in the event that it becomes advisable. Accordingly, on 31 December 2018, $550,000,000 of short-term notes payable have been classified as long-term debt.

Example

Classification of Liabilities and Date of Maturities FAQs

The notes payable would be classified as non-current. It is important to realize that not all companies have current liabilities, but they must have at least one non-current liability by virtue of the fact that their operating cycle will always be longer than 12 months.

The accounts payable would also be classified as non-current. It is important to realize that not all companies have current liabilities, but they must have at least one non-current liability by virtue of their operating cycle will always be longer than 12 months.

The accrued expenses will be classified as current liabilities because at some point they must be paid in order for the business to continue its operations. While not all companies have any current liabilities, they must have at least one by virtue of their operating cycle must always be longer than 12 months. They may have more than one and they may also have less than one if the company is reporting an operating loss.

The unearned revenue will also be classified as current liabilities because at some point the money must be collected in order for the business to continue its operations. While not all companies will have current liabilities, they do have to have at least one by virtue of their operating cycle must always be longer than 12 months. They may have more than one and they may also have less than one if the company is reporting an operating loss.

There are two parts to this question. First, how do we determine if a liability can be canceled? If the agreement contains language such as “the party agreeing to provide financing must be capable of honoring the agreement.”, then it cannot be canceled by the company who is providing the financing. The second part of this question is what happens to a liability once its stated maturity date has passed? It will either revert to current or become non-current based on whether the business still has an outstanding obligation to honor that debt.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.