In the weighted average cost method, the average cost of materials purchased is charged to the job or process rather than the actual cost. In other words, it is assumed that where a material is purchased at different prices, the unit cost will be the average cost of all units purchased over a particular period. The weighted average cost method follows the concept of total stock and total valuation. This method of material costing is used for costing materials requisition and charging the cost of materials to production. The balance on hand is also composed of units valued at the weighted average cost. For example, suppose 50 units of Material X are purchased at $10 per unit. Suppose that, a month later, another 50 units of Material X are purchased at $12 per unit. The cost to be charged to the job, process, department for Material X is $11 per unit (i.e., the average cost). To find the average price, the total cost of all materials of a particular class is divided by the number of units in hand. When new materials are purchased, the average price is calculated as follows: One formula for weighted average cost is given as follows: Another version of this formula is shown below: When using both of the above formulas, students are advised to calculate average cost and round to five decimal places. Materials are issued from the store at the established average cost until a new purchase is recorded. Although a new average price may be computed when materials are returned to sellers. When excess issues are returned to the store, it seems sufficient for practical purposes to reduce or increase the total quantity and cost, allowing the unit price to remain unchanged. This means that materials returned to sellers and to the store are recorded at the present average cost. The main advantages of the weighted average costing method include: The main disadvantages of the weighted average costing method include: Consider the following information: Determine the cost of inventory on 30 April using the weighted average method of costing.Weighted Average Cost: Definition

Weighted Average Cost: Explanation

Formula for Weighted Average Cost

Advantage of Weighted Average Cost Method

Disadvantages of Weighted Average Cost Method

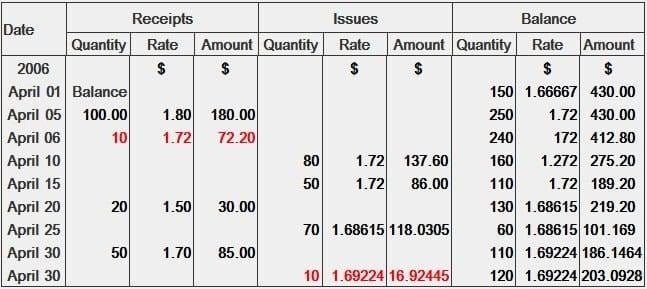

Example

Solution

Weighted Average Method of Material Costing FAQs

The weighted average cost is the average cost of all units purchased over a particular period.

The weighted average cost method follows the concept of total stock and total valuation. This method of Material Costing is used for costing materials requisition and charging the cost of materials to production. The balance on hand is also composed of units valued at the weighted average cost.

To find the average price, the total cost of all materials of a particular class is divided by the number of units in hand. When new materials are purchased, the average price is calculated as follows: 1. Add the quantity of units purchased to the quantity of units on hand 2. Add the cost of newly purchased materials to the cost of materials on hand 3. Divide the total cost (step 2) by the total quantity (step 1)

One formula for weighted average cost is: cost of units already in hand + cost of newly purchased units / units already in hand + newly purchased units another version of this formula is: weighted average unit cost = total cost item / total units of item

The main advantages of the weighted average costing method include: - minimizes the effect of unusually high and low material prices - practical and suitable for charging the cost of materials used to production - enables management to analyze operating results - simple to apply when receipts for materials are not numerous

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.