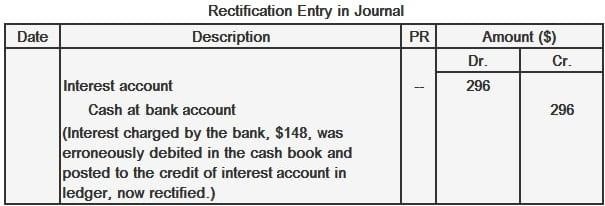

If a recorded transaction shows that both accounts have the correct debits and credits, the debit and credit entries in the ledger align and the trial balance remains unaffected. The debited account is credited and the credited account is debited. The correct entry should have twice the amount to erase the effect of the incorrect entry and establish the correct entry. Interest charged by the bank, $148, was entered in the debit side of the cash book and posted to the credit of the interest account.Explanation

Effect on Accounts

Rectification Entry

Example

Complete Reversal of Entries FAQs

After complete reversal of entries, the company's cash book will show a debit balance instead of a credit balance and that too double the actual amount. Now, if we follow this formula, then the credit balance should be double of the debit balance which means $6912 should be the answer.

By using the complete reversal of entries method, we will get an idea about the errors in transactions and we will be able to pinpoint which transaction is wrong.

The numerical value of an account's balance is also affected by debit and credit treatment. For example, if there is a $10 debit balance in an account, it means that it has a negative balance and its total assets are lower than its total liabilities. By contrast, a credit balance means that the account's assets are greater than its liabilities.

Partial reversal means undoing only a portion of transactions while complete reversal means undoing all the transactions done in error. Thus, it becomes necessary to reverse all transactions because we can't undo some and leave other as they are as this will affect other future transactions as well.

A reversing entry can be termed as journal entry which is used for recording transactions after accounting errors.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.