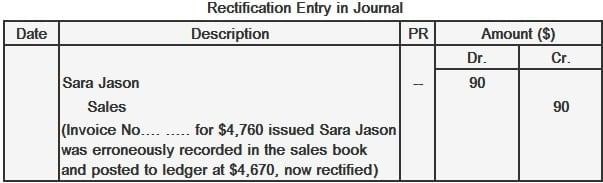

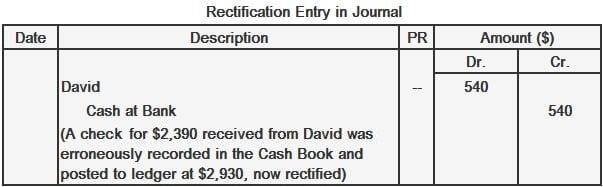

If a transaction is recorded in the subsidiary book with the incorrect amount, both the debit and credit entries made subsequently in the ledger will be incorrect despite being equal in terms of figures. Of course, this will not affect the trial balance. The effect on accounts will be either one of the following: If a transaction is recorded at less than the correct amount: If a transaction is recorded in the subsidiary book at more than the correct amount: An invoice issued to Sara Jason for $4,760 was entered into the sales book at $4,670 and posted to the ledger accordingly. As such, the account was under-debited by $90, while the sales account was under-credited by the same amount. A check for $2,390 was received from David. It was recorded in the cash book and posted to the ledger at $2,930. This means that the cash at bank account was over-debited and David's account was over-credited by $540.Explanation

Effect on Accounts

Rectification Entry

Example

Errors in Original Entry FAQs

If a transaction is recorded in the subsidiary book with the incorrect amount, both the debit and credit entries made subsequently in the ledger will be incorrect despite being equal in terms of figures. Of course, this will not affect the Trial Balance.

If the recorded transaction is more than the correct amount, the relevant ledger accounts will be over-debited and over-credited. If it is less than accurate, they will be under-debited and under-credited.

Errors in original entry are identified when a transaction recorded in the subsidiary book is posted to a wrong account or in a wrong column in the ledger. The amount will not tally with that of the initial transaction and subsequent entries made afterwards in the same journal or subsidiary books.

The errors in original entry will be adjusted through a debit or credit memo. It is then posted to the relevant accounts in the ledger.

Errors in posting occur when financial transactions are recorded incorrectly either in the journal or subsidiary books. As well as being incorrect, these figures affect all subsequent entries made in the ledger.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.