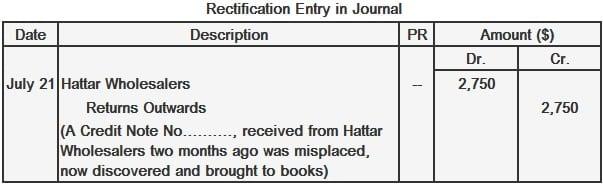

When some transactions are completely omitted from the books of accounts or entered but not posted, they are treated as errors of omission. If a transaction is omitted altogether from the books of accounts, there would be neither a debit nor a credit entry in the ledger. Hence, the trial balance will not be affected. There are two types of errors of omission: The transaction is recorded in the books but not posted to the ledger. This type of error can happen in any subsidiary book. For example, goods purchased and returned to the supplier may be entered in the purchase returns book but not posted in the debit of supplier account. The transaction is completely omitted from being recorded in the books. For example, a transaction relating to the receipt of cash may not be recorded in the cash book. Partial omissions are easy to locate, but this is not the case with complete omissions. One can only learn about such errors when the statement of accounts is received from or sent to creditors or debtors, as the case may be. The ledger will have no record of the transaction because there will be no debit or credit entry in the ledger. The transaction is recorded in the general journal in the same way that it would have been recorded when it originally took place. The reason for the delay is given in the narration. A credit note for $2,750, received from Hattar Wholesalers, was misplaced and not recorded in the books. It was discovered two months later on 21 July 2017. For this reason, the following rectification entry was made in the journal.Errors of Omission: Definition

Types of Errors of Omission

Partial Omission

Complete Omission

Effect on Accounts

Rectification of Entry

Example

Errors of Omission FAQs

When some transactions are completely omitted from the books of accounts or entered but not posted, they are treated as errors of omission.

The best way to determine if you have made an error of omission is to carefully check your work for any missing information. If you are unsure about something, ask a friend or colleague for help.

The transaction is recorded in the books but not posted to the ledger. This type of error can happen in any subsidiary book.

The transaction is completely omitted from being recorded in the books. For example, a transaction relating to the receipt of cash may not be recorded in the cash book.

The consequences of an error of omission can be serious, as it can result in misleading or inaccurate financial statements. It is important to rectify any errors as soon as they are discovered.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.