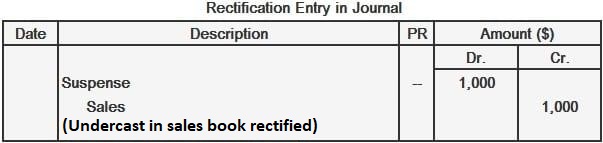

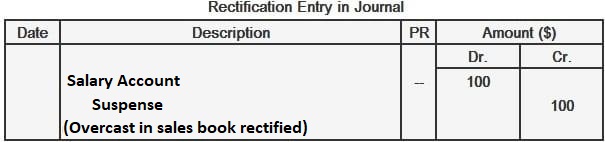

If a subsidiary book is miscast (i.e., wrongly totaled), the account to which its total is posted in the ledger would show an incorrect amount, whereas the individual accounts posted from the subsidiary book would add up to a different but accurate figure. Suppose that a company's sales book is undercast by $1,000. The correct total in the sales book is meant to be $79,400. This means that the sales account in the ledger has been credited at $78,400, whereas the individual debtors have been debited with a total of $79,400 (i.e., the correct total of individual invoices). As a result, the trial balance will show a difference of $1,000, with the debit side having a larger total. Suppose that a company's sales book is overcast by $100. The correct total is meant to be $36,400. This means that the sales account in the ledger has been credited at $36,500, whereas the individual debtors have been debited with a total of $36,400. As a result, the trial balance will show a difference of $100, with the credit side having a larger total.Example: Undercast Subsidiary Account

Example: Overcast Subsidiary Account

Miscast Subsidiary Account FAQs

Miscast is a transposition error in the subsidiary book, which means that postings are of an incorrect amount.

A sales book might be miscast if it were undercast or overcast. An Accounts Receivable book might be miscast if debit balances are posted on the credit side of the ledger and vice versa.

A book might be miscast because of an unintentional transposition error, such as one made by a clerk when posting to the ledger. That same clerk might also make an arithmetic error in totaling entries that could potentially lead to miscasting.

A miscast report helps identify if the books have been miscast by going over each account and identifying postings that have been posted in the wrong column.

One way to fix this kind of error is to go back to the source documents. If this isn't possible, you would need to rectify the problem manually. This involves summarizing all of the information in a Trial Balance and then making corrections based on that information.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.