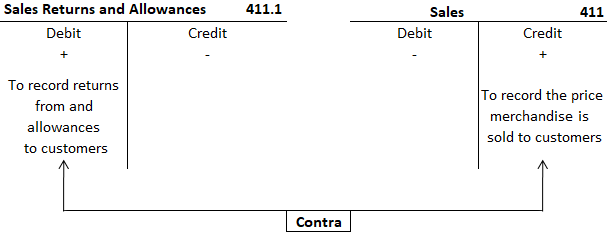

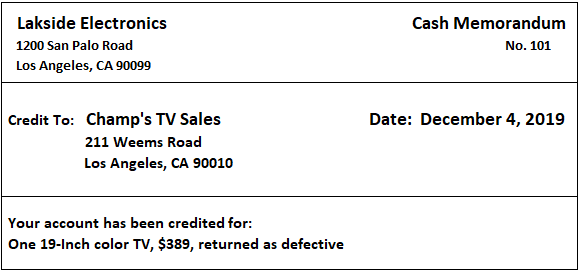

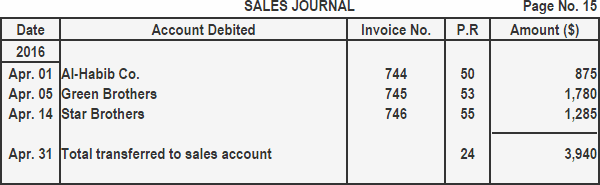

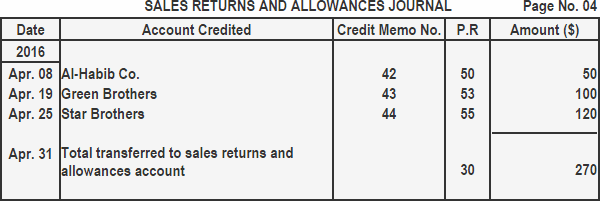

Sales returns and allowances is a contra revenue account with a normal debit balance used to record returns from and allowances to customers. The account, therefore, has a debit balance that is opposite the credit balance of the sales account. When sales are returned by customers or an allowance is granted to them due to delayed delivery, breakage, or quality issues, an entry is made in the sales returns and allowances journal. Return of merchandise sold for cash is entered in the cash payments journal or cash book. A return occurs when a buyer returns part or all of the merchandise they purchased back to the seller. An allowance occurs when a buyer decides to keep damaged or defective goods but at a reduction from the original price. In the seller’s books, a return or allowance is recorded as a reduction in sales revenue. Since the sales account normally has a credit balance, returns and allowances could be recorded on the debit side (the reduction side) of the sales account. However, to improve the bookkeeping process, returns and allowances are often recorded in a separate account entitled sales returns and allowances. When merchandise is returned by a customer or an allowance is granted, a credit memorandum (also known as a credit memo) is prepared. The credit memo is prepared in duplicate. The original memo is sent to the customer and the duplicate copy is retained. Credit memos serve as vouchers for entries in the sales returns and allowances journal. Like debit memos, all credit memos are serially numbered, as shown below. Goods sold on credit are often returned to the seller on the understanding that the customer’s account will be credited (reduced) by the amount of the return. The seller usually issues the customer a credit memorandum showing the amount of credit granted and the reason for the return. On the books of the seller, the customer’s accounts receivable account has a debit balance. Thus, the term credit memorandum indicates that the seller has decreased the customer’s account and does not expect payment. To illustrate, suppose that Lakeside Electronics issued the credit memorandum shown in the figure below to Champ’s TV Sales for the return of a defective 19-inch TV. Lakeside used the credit memorandum in the above figure as a source document for the following general journal entry. The credit part of this entry involves both a controlling account (accounts receivable) in the general ledger and a customer’s account (Champ’s TV Sales) in the accounts receivable subsidiary ledger. Debits or credits to a controlling account require a dual posting to the controlling account in the general ledger and to the customer’s account in the accounts receivable ledger. To indicate that dual posting is necessary, a diagonal line is drawn in the P.R. column of the journal at the time the journal entry is made. When the above entry was posted to the accounts receivable ledger, a small checkmark was made to the right of the diagonal line. When posting to the accounts receivable controlling account, the account number of accounts receivable (112) was written to the left of the diagonal line. If a cash refund is made due to a sales return or allowance, the sales returns and allowances account is debited and the cash account is credited. Cash refunds are recorded in the cash payments journal. The format of the sales returns and allowances journal is shown below. 1. Date column: Used to record the date customers return merchandise. 2. Account credited column: Used to record the account title of the customer whose account is credited for the return of merchandise. 3. Credit memo No. Column: Used to record the credit memorandum number related to the merchandise returned. 4. Posting reference column: Used to record the account number at the time of posting entries from the sales returns and allowances journal to ledger accounts. 5. Amount column: Used to record the amount of merchandise returned by the customer. Entries from the sales returns and allowances journal are posted to relevant accounts in the accounts payable subsidiary ledger and general ledger. The procedure is described below: Record the following transactions in the sales journal and sales returns and allowances journal, and post to the ledger accounts. Year: 2016 Sales Journal and Sales Returns and Allowances Journal: Accounts Payable Subsidiary Ledger: General Ledger:Sales Returns and Allowances: Definition

Sales Returns and Allowances Journal

Explanation

How to Record Sales Returns and Allowances

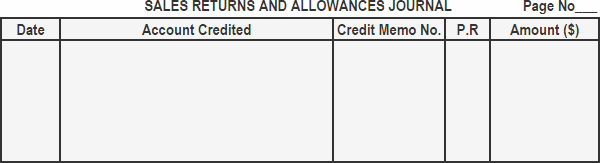

Format of Sales Returns and Allowances Journal

Posting Entries From Sales Returns and Allowances Journal to Ledger Accounts

Example

Solution

Sales Returns and Allowances FAQs

Since the ledger accounts are closed to the General Ledger, this account balance indicates that there are no more invoices in which credits have not been posted. Therefore, it means that all the customers’ accounts were paid.

Credit memo numbers are records that allow your company to track credits given for various issues. These memos may correspond to different customers, different reasons for the credit, or even multiple products/services which have been returned.

A control account allows you to easily follow the balances of related accounts by following the balance of the control account. The accounts that are related to each other (the ones with the same column heading) are said to be controlled by or linked to each other, and they share a common control account.

A contra-revenue account is a liability from revenue which helps in determining whether to omit certain sales transactions, which would otherwise be mistaken as revenue. It is usually included if there are any sales returns and allowances or other type of return not recorded in the sales journal.

Overshooting in sales is caused due to overstating of sales returns and allowances.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.