The accounting cycle begins with the analysis of transactions. The proper analysis of business transactions is important because it ensures that entries in the journal are correct. Analysis of business transactions involves the following four steps: Every business transaction involves two or more accounts. The process of analyzing a business transaction starts with identifying these accounts. For example, suppose that Mr. John starts a business with cash amounting to $25,000. This is a transaction that involves two accounts: namely, the cash account and the capital account. The second step of transaction analysis is to ascertain the nature of the accounts identified in the preceding step. In the above example, cash is an asset account and capital is an owner’s equity/capital account. Consider learning more about the classification of accounts. After ascertaining the nature of the accounts, it is necessary to determine which account is increasing and which one is decreasing as a result of the transaction. This is necessary for the proper application of rules of debit and credit on each account. In the above example, the two accounts involved are the cash account and capital account, both of which are increasing. The final step involved in transaction analysis is to apply the rules of debit and credit on accounts. In this step, we determine which account is to be debited and which one is to be credited on the basis of the increase and decrease in accounts identified in the preceding step. Using the same example, the cash account would be debited because, when an asset increases, its account is debited. The other account involved is John’s capital account, which would be credited. This is because the capital account is credited when capital increases. Consider the following information: Required: Give a stepwise analysis of the above transactions.What are the Steps of Transaction Analysis?

Ascertaining the Accounts Involved

Ascertaining the Nature of Accounts

Determining the Effects in Terms of Increase and Decrease

Applying the Rules of Debit and Credit

Example

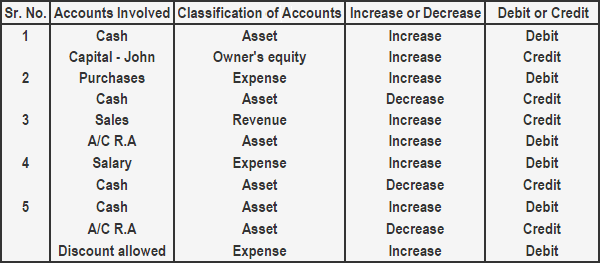

Solution

Analysis of Business Transactions FAQs

The Accounting Cycle begins with the analysis of transactions. The proper analysis of business transactions is important because it ensures that entries in the journal are correct.

Analysis of business transactions involves the following four steps:- ascertaining the accounts involved in the transaction- ascertaining the nature of the accounts involved in the transaction- determining the effects (i.E., In terms of increases and decreases in the accounts)- applying the rules of debit and credit

Every business transaction involves two or more accounts. The process of analyzing a business transaction starts with identifying these accounts.

Accounts are classified using two approaches:- traditional approach - modern approach

After ascertaining the nature of the accounts, it is necessary to determine which account is increasing and which one is decreasing as a result of the transaction. This is necessary for the proper application of rules of debit and credit on each account.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.