The term working capital refers to the portion of total capital that is used to run a business efficiently and regularly. It is also known as short-term capital, circulating capital, or liquid capital. Working capital can also be viewed as the current assets minus the current liabilities of an organization. It is also known as the net current assets. Working capital, in other words, means management of current assets: namely, cash in hand, cash at bank, bills receivable, closing stock, and debtors. It also means management of current liabilities, including sundry creditors, bills payable, outstanding creditors, bank overdraft, and so on. A company's working capital is its total current assets minus its current liabilities. The problem of working capital management involves the problem of decision-making regarding investment in current assets with an objective of maintaining liquidity of funds to enable the firm to meet its payment obligations as and when due. Noteworthy definitions of working capital published by previous authors and researchers are: The basic objectives for which a business unit needs working capital are: The management of working capital is useful for day-to-day finance for a business. Proper cash management is needed for every unit. Without this, the business will experience many problems, including the lack of cash to pay creditors and suppliers. Working capital is needed to make payments for the day-to-day expenses of the organization, as well as to cover the organization's financial requirement between the gap period of production to sales. Working capital is also essential for maintaining the liquidity of the organization. The following formula is used to calculate working capital: Working capital = Current assets - Current liabilities To manage working capital effectively, it is necessary to overcome the following challenges: 1. Availability of Cash Discount: When sufficient cash balance is maintained, the firm can benefit from cash discounts by paying in cash to purchase materials and other fixed assets. 2. Safety to Creditors: Management will face less pressure if they have sufficient working capital because they can pay creditors on the due date, which increases the creditability of the firm. 3. Debt-Securing Capacity: When firms pay their creditors, their creditability increases, which elevates their capacity to raise funds from the market. As such, the firm can use purchase goods on credit and borrow short-term funds from the bank. 4. High Dividend Rate: When a firm has adequate resources, it can pay a high rate of dividends to shareholders. Projects are retained in business so that when the need for additional financing arises, the same can be applied. The following are the important techniques/methods of calculating working capital: The working capital cycle is the period that a business takes to convert cash that has been invested in goods back into cash. A business unit buys goods and keeps them for a period before they are sold (i.e., average stock retention period). In the case of a manufacturing business, the average stock retention period needs to be calculated for each type of stock (i.e., for raw materials, work-in-progress, and finished goods). After the finished goods are sold (frequently on credit), debtors take some time to pay for them (Average credit allowed period). The total time taken to achieve any of the following tasks represents the period taken by a business to collect its revenue from the point of purchasing raw materials to the point of receiving cash from debtors: However, since businesses also receive credit from suppliers (i.e., average credit received period), the actual period for which it funds its working capital is determined as follows: This indicator shows what portion of the total capital employed is held in the form of working capital. Clearly, a trading concern would have a larger portion of its capital employed in the form of working capital, while a manufacturing company would not. However, often the best indicator of a suitable division of capital employed between fixed assets and working capital is provided by the industry average.Working Capital: Definition

Working Capital: Explanation

Scholarly Definitions of Working Capital

Why Do Firms Need Working Capital?

Formula For Working Capital

Challenges When Managing Working Capital

Objectives, Needs, and Importance of Working Capital

Techniques/Methods of Calculating Working Capital

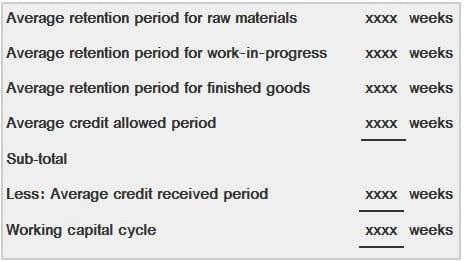

Working Capital Cycle

Working Capital as a Percentage of Capital Employed

Working Capital FAQs

Working Capital is the difference between current assets and current liabilities.

Cash, Accounts Receivable, marketable securities, inventories, prepaid expenses/expenses paid in advance, supplies on hand.

Accounts payable, accrued expenses/expenses paid in arrears, short term loans, deferred revenue.

A business with a higher sales to receivables ratio would have a higher Working Capital requirement. For example, an industry that generally has a 3:5 sales to receivables ratio would have a higher Working Capital requirement than an industry with a 1:1 ratio.

A business needs adequate levels of both long term liabilities and Working Capital to ensure that it has sufficient short-term liquidity, or cash in hand.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.